Food Price Inflation: What’s Really Happening at the Market

We analyzed three years of data to show you exactly which food categories saw the biggest increases and why.

Read ArticleHow inflation hits different income levels differently. We compare what RM1000 can actually buy depending on where you fall in the income spectrum.

We talk about inflation like it affects everyone equally. But that’s not how it works in reality. A 5% increase in food prices doesn’t hit a household earning RM3,000 monthly the same way it hits one earning RM8,000. The difference isn’t just about percentages — it’s about how much of your income goes to essentials.

When we look at purchasing power, we’re asking a simple question: what can your money actually buy? That answer changes dramatically depending on your income bracket. Lower-income households spend 50-60% of their money on food and basic needs. Higher earners? Usually 20-25%. So when food prices jump, the impact ripples through the economy in very different ways.

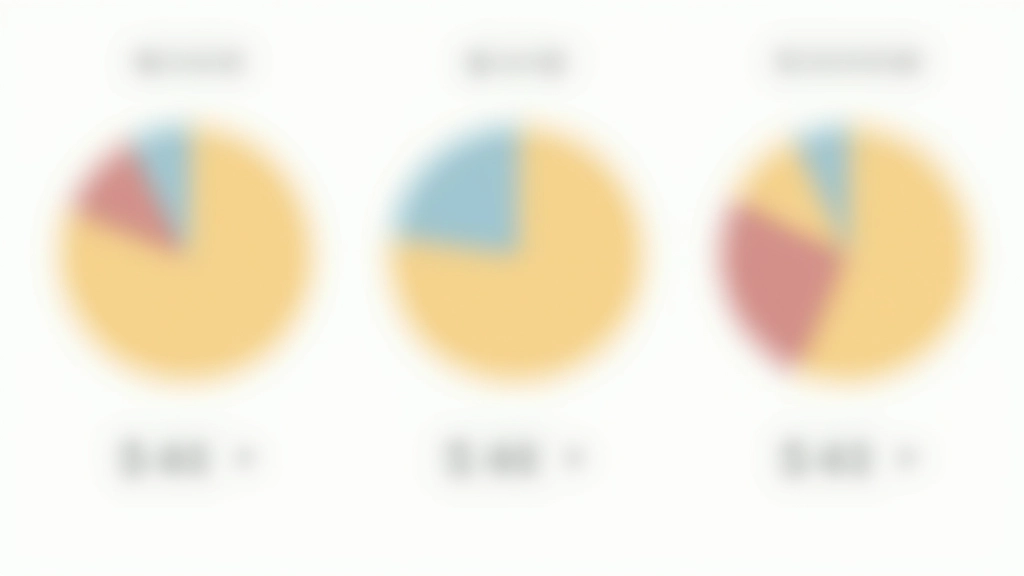

Let’s look at what happens with RM1,000 across different income groups. For someone earning RM2,500 monthly, that RM1,000 represents 40% of their income. For someone earning RM7,500 monthly, it’s only about 13%. The absolute amount is the same. The impact? Completely different.

RM2,500/month

RM1,000 covers: groceries (RM550), utilities (RM250), transport (RM200). Not much left for emergencies or savings. Price increases here are genuinely painful.

RM5,000/month

RM1,000 covers: groceries (RM450), utilities (RM200), transport (RM150), entertainment (RM150), plus some savings. Price increases are noticeable but manageable.

RM8,000/month

RM1,000 is discretionary spending. Premium groceries, dining out, entertainment. Price increases have minimal impact on essential needs or overall budget.

Food prices have been rising steadily. We’re not talking about restaurant prices — those are discretionary. We’re talking about staples. Rice, cooking oil, eggs, chicken, vegetables. Between 2022 and 2025, basic food items saw increases ranging from 8% to 18% depending on the category.

For lower-income households, this isn’t a minor inconvenience. When you spend RM550 monthly on groceries for a family, an 15% increase means an extra RM82.50 you didn’t have in the budget. That’s real money. Middle-income households feel it, but they’ve usually got some flexibility. Higher earners? They might not even notice because they’re already buying premium brands.

Key insight: Lower-income groups spend roughly 30-35% of their food budget on just three categories: rice, cooking oil, and protein. When these items spike, there’s nowhere to cut.

Where your money actually goes, by income bracket

The pattern is clear: lower-income households have much less flexibility. They’re already spending most of their income on necessities. When prices rise, they can’t easily cut back. Middle and higher-income groups have more room to adjust — they might eat out less, defer some purchases, or shift to different products.

Inflation isn’t neutral. It doesn’t affect everyone the same way. When food prices rise 15%, a high-income household might shift to a different brand of olive oil. A low-income household might have to choose between buying enough food and paying rent on time.

The data from household expenditure surveys shows this clearly. Lower-income groups have virtually no savings buffer. Around 72% of households earning RM2,500 monthly report having less than one month of expenses in emergency savings. For those earning RM7,500+, that number drops to 18%. So when prices spike, lower-income households can’t absorb the shock.

“When your income is tight, inflation isn’t just a number on a chart. It’s the difference between buying fresh vegetables or just rice for the week. It’s choosing between three meals and two.”

— Economic impact analysis, Malaysia 2025

This matters for policy, for businesses, for understanding how economies actually function. When purchasing power drops for lower-income groups, they spend less on everything except absolute necessities. Consumer spending contracts. Retail struggles. Unemployment can follow. It’s not just about individual hardship — it’s systemic.

A 10% price increase affects lower-income households dramatically but higher earners barely notice. The percentage is the same, but the real impact is completely different.

Lower-income households spend 50-60% on food and housing. There’s no room to cut. Middle and higher earners have flexibility that creates a buffer.

Over 70% of lower-income households have minimal emergency savings. They’re one price spike away from real hardship. Building financial cushion is crucial.

For lower-income groups, tracking food prices isn’t optional — it’s essential. Small percentage increases translate to real money that impacts monthly budgets.

This article presents informational and educational content about purchasing power, inflation, and household expenditure patterns in Malaysia. The data, statistics, and analysis are intended to help readers understand economic concepts and trends. They’re not financial advice, investment guidance, or personal recommendations. Circumstances vary widely between households and individuals. If you’re facing financial hardship or need specific guidance about your personal situation, we encourage you to consult with financial advisors, economists, or relevant government assistance programs. Prices, economic conditions, and policy frameworks change regularly, and information here reflects 2026 conditions. Always verify current data with official sources like the Department of Statistics Malaysia before making decisions based on economic data.